Your paycheck is lying to you - here's how to read it

How to Read Your Pay Stub: Every Line Item Explained

Most Americans get paid every two weeks and glance at their pay stub for about three seconds before moving on. They see the net pay number, confirm it landed in their bank account, and forget the rest. That works fine until it doesn't - until they notice something looks off, wonder why their take-home dropped, or realize they have no idea what half those line items mean.

This guide fixes that. Every major section of a standard pay stub, explained in plain English - no accounting degree required.

Before you dig in: if you want to see how all of these pieces add up for your specific situation, run your numbers through the free State Pay Calculator. It breaks out federal, state, and FICA taxes by state so you know exactly where your money is going.

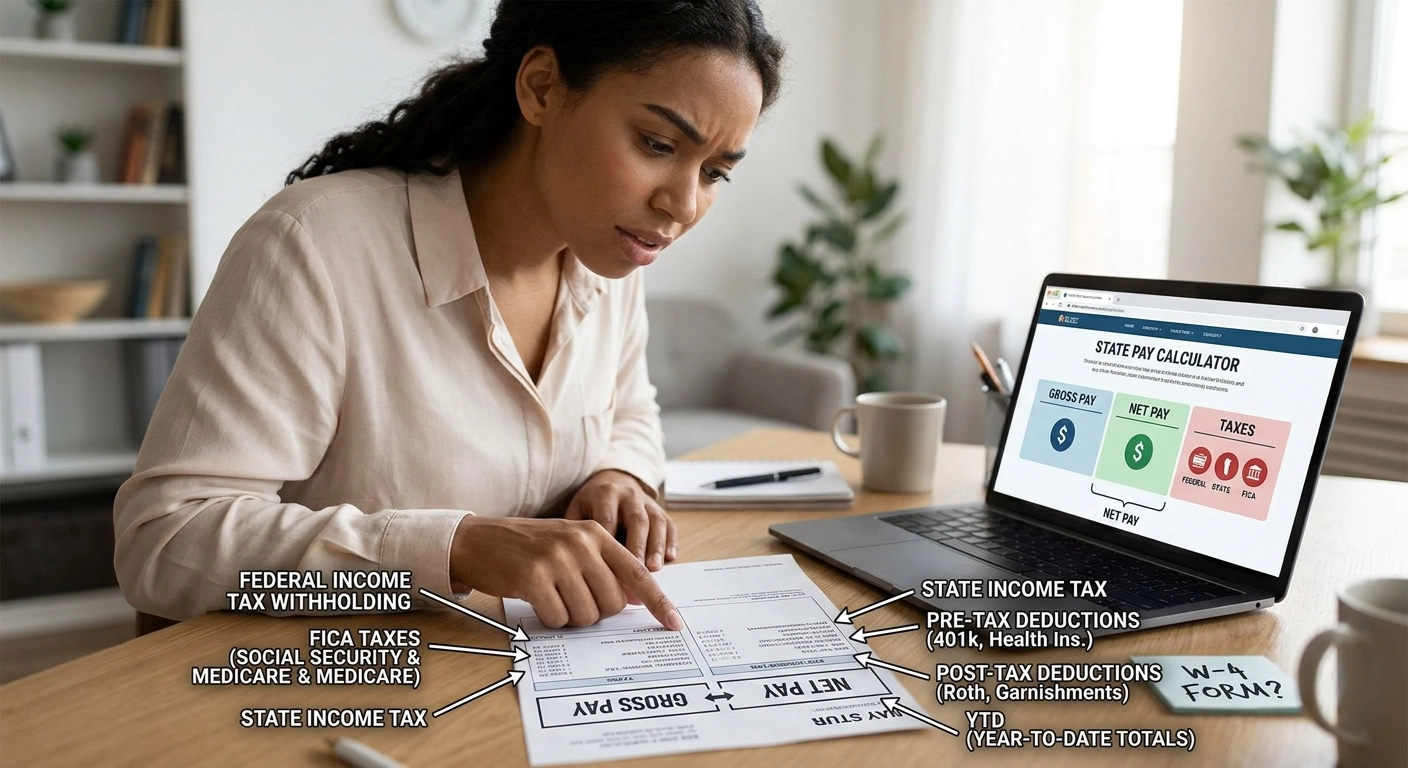

The Big Picture: Gross Pay vs. Net Pay

Start here. Everything else on your pay stub is just the math between these two numbers.

Gross Pay is what you earned this pay period - before anything is taken out. If you're salaried at $60,000/year and paid biweekly, your gross pay each check is $2,307.69. If you're hourly, it's your hours worked times your rate, plus any overtime.

Net Pay is what actually hits your bank account. It's your gross pay minus every deduction below. This is also called your "take-home pay."

The gap between these two numbers is where most people get confused. Let's close it.

Federal Income Tax Withholding

This is typically the biggest deduction on your stub. The IRS doesn't wait until April to collect - they take a portion each pay period based on your W-4 form and the current federal tax tables.

Why does this number change sometimes? A few reasons:

You updated your W-4 (added a dependent, changed your filing status)

You received a bonus or overtime that pushed your annualized income into a higher bracket for that period

Your year-to-date earnings crossed a withholding threshold

It's normal for this number to vary slightly. If it seems wildly off - consistently too high or too low - it's worth revisiting your W-4. We'll cover that in the W-4 guide here on the blog.

FICA Taxes: Social Security and Medicare

FICA stands for Federal Insurance Contributions Act. It funds two programs: Social Security and Medicare. Unlike federal income tax, FICA doesn't depend on your W-4. It's a flat percentage, every check, no negotiating.

Social Security (OASDI) You'll often see this labeled "OASDI" on your stub - which stands for Old-Age, Survivors, and Disability Insurance. In 2026, the rate is 6.2% of your gross wages, up to a wage base of $176,100. Once you hit that ceiling for the year, Social Security withholding stops for the rest of the calendar year.

Medicare Medicare is withheld at 1.45% of all wages - no cap. If you earn over $200,000 ($250,000 for married filing jointly), an additional 0.9% kicks in under the Affordable Care Act.

Your employer matches both of these contributions on their end. You pay half; they pay half.

State Income Tax

If you live in a state with an income tax, you'll see this line on every stub. The rate varies significantly depending on where you work. California tops out at 13.3% for high earners. States like Texas, Florida, and Washington have no state income tax at all - so residents there simply don't have this line.

Want to see exactly how your state stacks up? The State Pay Calculator runs the numbers for all 50 states side by side.

Pre-Tax Deductions

These come out of your gross pay before taxes are calculated - which is what makes them valuable. Common pre-tax deductions include:

401(k) or 403(b) contributions - retirement savings that reduce your taxable income now

Health insurance premiums - if your employer offers a group plan and you enroll

FSA / HSA contributions - flexible or health savings accounts

Dental and vision premiums

Commuter benefits - transit passes or parking in qualifying plans

The more you put into pre-tax buckets, the lower your taxable gross becomes - which means less withheld for federal and state income tax.

Post-Tax Deductions

These come out after taxes are calculated. They reduce your net pay but don't affect your tax liability. Examples:

Roth 401(k) contributions - you pay taxes now, withdrawals in retirement are tax-free

Life insurance premiums (in some employer plans)

Wage garnishments - court-ordered deductions for things like child support or unpaid debt

Union dues

YTD: What It Means and Why It Matters

YTD stands for Year-to-Date. Most pay stubs show both the current period amount and the YTD total for each line item.

Your YTD column is useful for several things:

Tracking your Social Security wage base - once your YTD gross hits $176,100 in 2026, OASDI withholding stops

Reconciling with your W-2 at tax time - your YTD figures should match Box 1 (wages) and Boxes 4 and 6 (Social Security and Medicare withheld)

Spotting errors - if something looks wrong, the YTD column tells you how long it's been wrong

Other Lines You Might See

Depending on your employer and state, you may also see:

SDI (State Disability Insurance) - California, New York, New Jersey, Hawaii, and Rhode Island all have mandatory SDI deductions

SUI / SUI Employee - some states withhold a small amount for state unemployment insurance from employees

Local/City Tax - if you work in a city with its own income tax (Philadelphia, New York City, Columbus, Portland, etc.)

Employer HSA Contribution - some employers deposit money into your HSA; this shows up for informational purposes

Quick FAQ:

What is OASDI on my paycheck? OASDI is Social Security. It stands for Old-Age, Survivors, and Disability Insurance. In 2026, 6.2% of your wages up to $176,100 is withheld annually.

Why does my federal withholding change every check? It's recalculated each pay period based on your W-4, your year-to-date earnings, and the IRS withholding tables. Overtime and bonuses are common causes of fluctuation.

What does YTD mean on my pay stub? Year-to-Date. It's the running total of your earnings and deductions from January 1 through your most recent paycheck.

What's the difference between gross and net pay? Gross is what you earned. Net is what you take home after every deduction is subtracted.

Now You Know What You're Looking At

Your pay stub isn't complicated - it's just unfamiliar. Gross pay, federal withholding, FICA, state tax, pre-tax deductions, and your YTD totals. That's the whole picture.

If you want to see how these numbers would change with a different salary, a different state, or different withholding elections - run it through the State Pay Calculator. Free, no signup, all 50 states covered.

Frequently Asked Questions About Your Pay Stub

What is OASDI on my paycheck? OASDI stands for Old-Age, Survivors, and Disability Insurance - it's the official name for Social Security tax. In 2026, your employer withholds 6.2% of your gross wages for OASDI, up to the annual wage base of $176,100. Once your year-to-date earnings hit that ceiling, the deduction stops for the rest of the year.

Why does my federal withholding change every paycheck? Federal income tax withholding is recalculated every pay period using your W-4 elections, your year-to-date earnings, and the IRS withholding tables. The most common reasons it shifts: you received overtime or a bonus that temporarily pushed your annualized income into a higher bracket, your pay date fell in a way that affected the calculation, or you recently updated your W-4. Small fluctuations are normal. Large, consistent swings usually mean your W-4 needs attention.

What is the difference between gross pay and net pay? Gross pay is your total earnings before any deductions - taxes, benefits, retirement contributions, or anything else. Net pay is what actually lands in your bank account after all of those deductions are subtracted. The gap between the two is your total withholding burden for that pay period.

What does YTD mean on a pay stub? YTD stands for Year-to-Date. It shows the cumulative total of your earnings and each deduction category from January 1 through your most recent paycheck. Your YTD figures are important at tax time - the numbers on your W-2 should match your final YTD totals for the year.

What is FICA tax and why is it on every paycheck? FICA stands for Federal Insurance Contributions Act. It's the combination of Social Security (6.2%) and Medicare (1.45%) taxes - totaling 7.65% of your gross wages. Unlike federal income tax, FICA doesn't depend on your W-4. It's a flat rate applied to every paycheck with no exceptions. Your employer pays an equal 7.65% match on top of what you contribute.

What are pre-tax deductions and how do they affect my paycheck? Pre-tax deductions are amounts taken out of your gross pay before federal and state income taxes are calculated. Common examples include 401(k) contributions, health insurance premiums, FSA and HSA deposits, and qualifying commuter benefits. Because they reduce your taxable gross, pre-tax deductions lower your income tax withholding - meaning they cost you less out-of-pocket than the dollar amount suggests.

Why is there a state tax line on my pay stub - or why is it missing? If you live and work in a state with a state income tax, your employer withholds a percentage each pay period based on that state's rate and your withholding elections. Nine states - including Texas, Florida, Washington, and Nevada - have no state income tax, so residents there simply won't have that line on their stub. If you work in a different state than you live in, you may see withholding for both states, depending on reciprocity agreements between them.